Highlights of the 2020 Law - Individuals

As usual, this year brings a new batch of tax laws for business and individual tax returns. This post will outline some of the major changes for individuals. If you are looking for business tax changes you can go here.

Article Highlights

- Economic Impact Payments - First and Second Round

- Educator

Expense

- Unemployment

Assistance

- Earned

Income Tax Credit & Child Tax Credit

- Cash

Charitable Contributions for Non-Itemizers

- Charitable Contributions for Itemizers

- Flexible

Spending Arrangements Carryover

- Reduction

in Medical Deduction AGI Floor

- Education

Credits

- Volunteer Firefighters and Emergency Medical Responders

- Discharge of Qualified Principal Residence Indebtedness

- Student Loans

- Mortgage Insurance Premiums

- Housing Relief

- Energy Efficient Home Improvement Credit

- 2-Wheeled Plug-In Electric Vehicle Credit (Motorcycles)

- Alterative Fuel Vehicle Refueling Equipment Tax Credit

- Fuel Cell Vehicles

- Residential Solar Energy Equipment Tax Credit

- COVID-Related Tax Relief Act of 2020 (COVIDTRA) and

- Taxpayer Certainty and Disaster Tax Relief Act of 2020 (TCDTR).

The entire text of the Consolidated Appropriations Act of 2021--all 5,593 pages--can be found here.

This post provides an overview of some of the tax provisions in the legislation that will affect individual tax returns.

Economic Impact Payments - First and Second Round

As many of you are aware, CAA released a second round of economic impact payments (EIP) also referred to as stimulus payments. These payments are in addition to the stimulus payments issued throughout 2020 under the CARES Act passed in March 2020.

First round

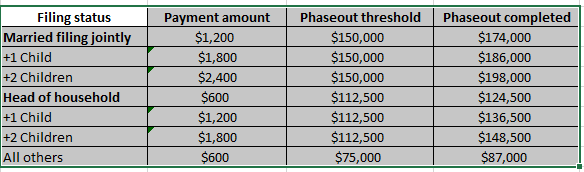

The first round of payments were $1,200 per eligible individual and $2,400 for married couples filing a joint return. There was an additional $500 for certain dependents based on the taxpayers' adjusted gross income for 2018 or 2019. The payments were reduced or phased out if AGI exceeded:

- $150,000 if married filing a joint return

- $112,500 if filing as head of household

- $75,000 if using any other filing status.

Second round

The second round of payments are $600 per eligible individual and $1,200 for married couples filing a joint return plus $600 for eligible dependents. These payments are also based on AGI as filed on the 2019 tax return. The payments will be reduced or phased out at the same rate if AGI exceeds the thresholds above.

Rebate amounts and phaseout ranges for second round

If the actual credit is higher than what was received (meaning the IRS did not send you enough), you will receive the difference as a refundable tax credit on the 2020 tax return. Both rounds of these recovery rebates are an advance of a refundable tax credit that will be calculated on the 2020 tax return. The actual credit amount will be determined based on your 2020 AGI and number of eligible dependents claimed. Once the actual credit amount is calculated on the 2020 tax return, it will need to be compared to the payments that were actually received during rounds one and two.

If the actual credit happens to be less than what was received, (meaning the IRS sent you too much), you will not have to pay the difference back. You just won't have any additional tax credit to claim on the the 2020 tax return.

New tax form Notice 1444 and 1444-B

The IRS mailed Notice 1444, Your Economic Impact Payment, to each taxpayer who was issued a recovery rebate during round one and will be issuing a similar Notice 1444-B to anyone who receives a payment during round two. In order to appropriately calculate any remaining credit you might be eligible for, it will be important for you to provide copies of these notices to us when submitting information for the 2020 tax returns.

Resources for more information

- "Get My Payment" to check the status of your payment and how it was sent to you.

- Information about the first round of payments, "Economic Impact Payment Information Center".

- FAQ about the second round of payments, "FAQ Second Economic Impact Payment"

Educator Expense

Eligible K-12 teachers and instructors are entitled to a

$250 annual above-the-line deduction for certain school-related expenses paid

out of their own pockets.

The CAA specifies that the $250 above-the-line educator expense deduction will include personal protective equipment (PPE), disinfectant, and other supplies used for the prevention of the spread of COVID-19 effective for expenditures after March 12, 2020.

Unemployment Assistance

All Federal supplemental unemployment insurance benefits, which had already

expired or would end on December 31, 2020, will be extended through March 14,

2021. However, the supplemental amount will only be $300 per week instead of

the $600 that the CARES Act authorized.

Earned Income Tax Credit (EITC) & Child Tax Credit (CTC)

The CAA includes a temporary change that could result in larger earned income tax credits (EITCs) and child tax credits (CTCs). It allows lower-income individuals to use their earned income from the 2019 tax year to determine their EITC and the refundable portion of their CTC for the 2020 tax year. This could produce larger credits for eligible taxpayers who earned lower wages in 2020 due to the pandemic.

Cash Charitable Contributions for Non-Itemizers

For 2020, the CARES Act allows non-itemizers to deduct $300 of cash

contributions regardless of filing status. The Act of 2020 changes that for

2021 and allows an above-the-line deduction for cash contributions of $600 for

joint filers and $300 for all other filing statuses. However, Congress is

concerned that taxpayers will abuse this provision and added a 50% underpayment

of tax penalty where the contribution cannot be properly documented. Cash

Charitable Contributions for Itemizers For 2020 the 60% limit on cash

contributions was suspended for 2020, thus allowing larger cash contributions

during the COVID crisis. Under the Act the suspension of the 60% limit has been

extended to 2021.

Charitable Contributions for Itemizers

Before 2020, you could not claim an itemized charitable

deduction for cash contributions to IRS-approved charities that exceeded 60% of

your adjusted gross income (AGI). The Cares Act suspended the AGI limit for

qualifying charitable contributions made in 2020.

The CAA extends this suspension into 2021.

Flexible Spending Arrangements Carryover

Under current law cafeteria plans may only permit a carryover of unused amounts

remaining in a health FSA as of the end of a plan year in an amount of no more

than $550.

The Act extends the carryover period to 12 months after the end of such plan

year for unused benefits and contributions to health flexible spending and

dependent care flexible spending arrangements for 2020 and 2021.

An employer may also allow an employee who ceases to participate in the plan

during calendar year 2020 or 2021 to continue to receive reimbursements from

unused benefits or contributions through the end of the plan year in which the

employee’s participation ceased, including any extended grace period.

Reduction in Medical Deduction AGI Floor

The Tax Cuts and Jobs Act (TCJA) set the threshold for itemized medical expense deductions at 7.5% of adjusted gross income (AGI). The threshold was scheduled to increase to 10% of AGI for 2021 and beyond.

The CAA makes the 7.5%-of-AGI threshold

permanent for 2021 and beyond.

Education Credits

Qualified taxpayers generally can claim an education tax break with the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC). Previously, though, the two credits were subject to different phaseout rules, with the AOTC available at a greater MAGI than the LLC.

Also, before the new law, taxpayers could claim a “higher education expense

deduction” for qualified tuition and related expenses.

The CAA adopts a single phaseout for both the AOTC and the LLC, effective for tax years beginning after December 31, 2020. The credits will phase out beginning at $80,000 for single filers and ending at $90,000. For joint filers, they will begin to phase at $160,000 and disappear at $180,000 as illustrated in the chart below.

|

Filing Status |

Phaseout

Range |

|

Unmarried

Filing Status |

$80,000

– $90,000 |

|

Joint

Filing Status |

$160,000

- $180,000 |

|

Married

Separate |

No

Credit Allowed |

Volunteer Firefighters and Emergency Medical Responders

Emergency workers who are members of a “qualified volunteer

emergency response organization” can exclude from gross income certain state or

local government payments received and state or local tax relief provided on

account of their volunteer services. This exclusion was due to expire at the

end of 2020, but the Act made it permanent.

Discharge of Qualified Principal Residence Indebtedness

Usually, if a lender forgives a debt, such as a mortgage, the forgiven debt generally counts as taxable cancellation of debt (COD) income for federal income tax purposes. However, an exception applies to COD income from cancelled mortgage debt that was used to acquire a principal residence. Under the exception, up to $2 million of COD income from principal residence acquisition debt that was cancelled in 2007-2020 qualified as a federal-income tax-free item ($1 million for married individuals who filed separately for those years).

The CAA extends this exception to cover principal residence mortgage debt that’s forgiven in 2021-2025. However, the maximum amount of forgiven debt that can be treated as tax-free for those years is reduced to only $750,000 ($375,000 for married individuals who file separately).

Student Loans

Educational assistance provided under an employer's qualified educational

assistance program, up to an annual maximum of $5,250, is excluded from the

employee’s income. The CARES Act expanded the definition of expenses to include

employer payments of the employee’s student loan debt. But this special

allowance was only available for payments made between March 27, 2020 through

December 31, 2020. The Act extends the exclusion for loan repayments made through

2025.

Mortgage Insurance Premiums

You can deduct as an itemized deduction the cost of premiums for mortgage insurance on debt to acquire, construct, or improve a first or second residence as deductible qualified residence interest. The deduction is phased out for higher-income individuals.

The CAA extends this break through 2021.

Housing Relief

The new law includes multiple types of relief for those

struggling with their housing costs. For example, the federal eviction

moratorium is extended through January 31, 2021. The CAA also offers rental

assistance for families affected by COVID-19. Eligible households can apply the

funds to rent, utilities and energy costs — including amounts in arrears.

Energy Efficient Home Improvement Credit

Since 2006 taxpayers have been able to claim a tax credit of up to $500 for the installation of certain energy-saving improvements to their existing homes. The dollar limits and

credit percentages have been modified several times since the credit first

became available.

The credit of 10% of the amounts paid or incurred by the taxpayer for qualified energy improvements to the building envelope (windows, doors, skylights, and roofs) of principal residences ranges from $50 to $300 for energy-efficient property including furnaces, boilers, biomass stoves, heat pumps, water heaters, central air conditioners, and circulating fans, and is subject to a lifetime cap of $500. If you have already claimed the credit for an earlier year, you may not be eligible for any further credit.

The Act extends this credit through 2021.

2-Wheeled Plug-In Electric Vehicle Credit (Motorcycles)

You can claim a 10% federal income tax credit for the purchase of a qualifying electric-powered 2-wheeled vehicle manufactured primarily for use on public roads (i.e., electric-powered motorcycles). The credit can be worth up to $2,500. Battery capacity within the vehicles must be greater than or equal to 2.5 kilowatt-hours.

The CAA extends this credit for one year so that it applies to property purchased through 2021.

Alternative Fuel Vehicle Refueling Equipment Tax Credit

You can claim a federal income tax credit for up to 30% of

the cost of installing non-hydrogen alternative fuel vehicle refueling

equipment. For your Tesla or other electric vehicle.

The CAA extends this break to cover qualifying 2021 expenditures.

Fuel Cell Vehicles

You can claim a federal income tax credit for vehicles

propelled by chemically combining oxygen with hydrogen to create electricity.

The base credit is $4,000 for vehicles weighing 8,500 pounds or less. Heavier

vehicles can qualify for credits of up to $40,000. An additional $1,000 to

$4,000 credit is available to cars and light trucks to the extent their fuel

economy meets federal standards.

The CAA extends this credit to cover

qualifying 2021 purchases.

Residential Solar Energy Equipment Tax Credit

You can claim a generous federal income tax credit for qualifying solar energy equipment expenditures for your home. For equipment placed in service in 2020, the credit rate is 26%. The rate was scheduled to drop to 22% for equipment placed in service in 2021 before vanishing entirely for 2022 and beyond.

The CAA extends the 26% credit rate to cover equipment placed in service in 2021 and 2022 and extends the 22% rate to cover equipment placed in service in 2023. For 2024 and beyond, the credit is scheduled to vanish.

The

Act extends the credit phaseout for two years as illustrated in the table.

If you have any questions about the information discussed here just drop us a line.

For the latest tax updates be sure to follow us on Twitter, Facebook and LinkedIn. You can also visit our website at https://arndtcpas.com or give us a call at (417) 882-9000.

f you have questions about how this COVID-19 tax legislation might apply in

your situation, please give this office a call.