8 Scenarios on How the Tax Bill Will Affect You

We have just seen the biggest tax overhaul in 30 years.

The final version

rewrites the tax code in dozens of ways, eliminating deductions, changing

rates, and creating brand new benefits for certain taxpayers, such as business

owners.

With 479 pages of brand new tax law how can you know how the tax bill will affect you and your family?

How exactly would

these changes affect me?

It depends on where you live, what you do and how big

your family is. You're more likely to get a tax increase if you live in a

high-tax state or lean heavily on deductions—such as unreimbursed employee

expenses—that will be eliminated under the bill.

To see how Americans fare across

different incomes and circumstances, Bloomberg turned to Tim Steffen, director

of advanced planning at Baird Private Wealth Management.

His eight

scenarios examine only 2018 wage and pass through income from an S corp or partnership that you own and how taxes owed on those earnings would change when tax time comes

around in 2019.

The

Multimillionaires in New York

These Manhattan

residents have a jumbo mortgage (at an assumed 4 percent interest rate) and

take a $40,000 deduction on mortgage interest; pay property taxes of $96,250

and state income tax of $135,360; and make annual charitable contributions

totaling $100,000.

They will pay a

bit more next year because they would lose key deductions, especially the

ability to put down more than $10,000 in state and local taxes. That offsets a

drop in the top marginal tax rate, from 39.6 percent to 37 percent. (The

“marginal rate,” the rate paid on any extra dollar earned, is different from

the “effective tax rate,” which is the overall, blended rate you pay as

different tax rates are levied on your income at different thresholds.)

City taxes for

these Manhattan dwellers would work out to almost 4 percent. Combine that with

the top federal rate and top state rate, and you get a marginal rate

approaching 50 percent.

The Second-Home

Scenario in California

A married couple

has a primary residence in Malibu, California, and a second home in Lake Tahoe.

The property tax on the Malibu home is $15,860, and they pay $4,896 on their

second home; they deduct a total of $40,000 in mortgage interest for the two

homes; and they give $50,000 to charity.

This couple would

lose almost $86,000 in deductions under the tax bill. Nonetheless, other

changes—especially the drop in the top tax rate—means their effective tax rate

creeps up by only 0.5 percentage points.

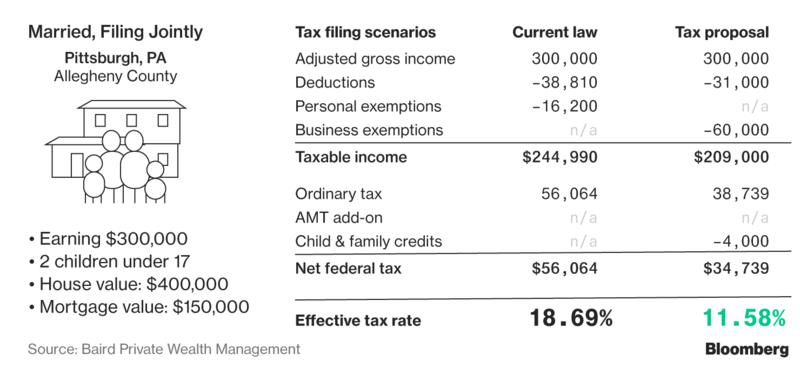

The Small

Business Owners in Pittsburgh

This married

couple with a small manufacturing business in Pittsburgh has $300,000 in

pass-through business income. Their deductible mortgage interest adds up to

$6,000; their property tax is $8,600; and they give 5 percent of their income

to charity.

These taxpayers

get a big benefit from the new 20 percent deduction aimed at pass-through

business owners, who pay their business income taxes through their individual

tax returns.

The Suburban

Family in Westchester

A married couple

in a New York suburb has estimated state income tax of $17,290; their annual

mortgage interest deduction is $14,000; and they pay property tax of

$13,750—about the same amount they donate to charity.

While the bill

takes a bite out of this family's deductions and exemptions, they would benefit

from enhanced child tax credits and avoiding the alternative minimum tax, or

AMT.

Single in

Manhattan

This New York

renter pays estimated state income tax of $8,148 and gives about $6,500 to

charity.

The final tax

legislation is more generous to this taxpayer than the bills that originally

passed the House and Senate. That's because it permits the deduction of state

and local income taxes up to $10,000. The original proposals scrapped the

income tax deduction entirely and allowed only a $10,000 deduction for property

taxes, which this renter doesn't pay.

Married in

Austin

This young couple

rents and has income of $100,000. They give $5,000 a year to charity.

The bill

eliminates the personal exemption, an automatic $4,050 deduction for each

family member. But for this couple, that loss is offset by rate cuts and a

near-doubling of the standard deduction, from $12,700 to $24,000 for married

couples.

Median Income

in Oregon

This Portland,

Oregon, couple earns close to the median household income for the U.S. Their

property tax bill is $1,688; their deductible mortgage interest is $3,000; and

their estimated state income tax is $4,744.

Because this

couple has few deductions, they benefit from the higher standard deduction,

netting a 2018 tax cut of $949.

Renting in

Milwaukee

This married

couple rents and has an estimated 2017 state income tax bill of $2,104.

This family ends

up with negative income tax rate, because they benefit from the enhanced child

tax credits, which are refundable. That means that, subject to limits,

low-income taxpayers are able to get larger refunds than they pay in income

taxes.